05 Position

Overview

In the previous chapter, we analyzed the complete process of swap price progression:

- price moves continuously on the curve

- Liquidity changes discretely at ticks

- The entire process is driven by a while loop

This liquidity comes from the positions of all LPs. Therefore, if swap describes how prices move, then Position describes where liquidity comes from.

In V3, an LP does not simply "put money into the pool"; instead, it provides liquidity over a price range for a period of time. A Position can be abstracted as:

(liquidity, tickLower, tickUpper)

liquidity: The amount of liquidity provided within this rangetickLower: lower bound of the intervaltickUpper: Upper bound of the interval

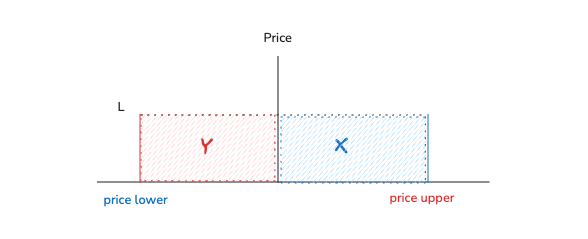

1. The relationship between Position and price

Whether a Position participates in a transaction depends only on whether the current price is within the range.

Case 1: The price is within the range

tickLower ≤ currentTick < tickUpper

at this time:

- The position provides liquidity

- It participates in the swap

- It can earn fees

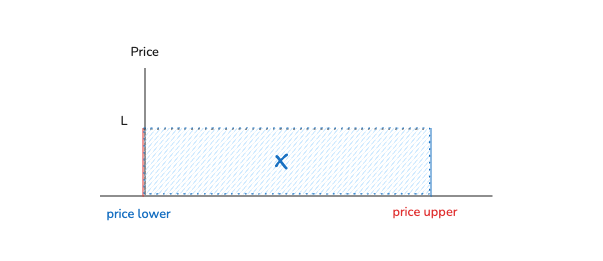

Case 2: Price is below the range

currentTick < tickLower

at this time:

- The position does not participate in the swap

- The asset is fully represented as token0

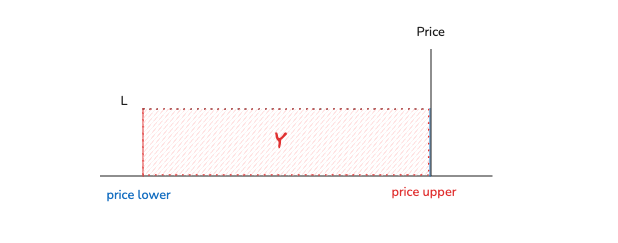

Case 3: Price is higher than the range

currentTick ≥ tickUpper

at this time:

- The position does not participate in the swap

- The asset is fully represented as token1

2. How Position constitutes the liquidity of the pool

In V3, within a certain price range, the current effective liquidity equals the sum of the liquidity of all active positions. Therefore, swap does not interact with a single LP, but with the aggregated liquidity of all LPs in the current range.

When the swap price advances, a tick crossing occurs when the price reaches a tick, and liquidity changes as well. The corresponding code is liquidity += liquidityNet. In fact, liquidityNet comes from the position that starts or ends at this tick.

liquidityNet = Σ (liquidity changes for all Positions that start or end at this tick boundary)

So, in essence, a tick is the boundary of a position, liquidityNet is the liquidity change at that boundary, and swap moves the price across the liquidity formed by positions.

3. Open position: mint

The process of creating a position is actually to convert tokens into liquidity and bind that liquidity to a price range. The mint function in the NPM (Nonfungible Position Manager) contract does three things:

- Determine the price range (tickLower / tickUpper)

- Calculate liquidity based on current price and range

- Transfer the corresponding amount of token0/token1

The actual process provides users with amount0Desired/amount1Desired, then calculates the maximum supported liquidity based on the current price and range, and then returns or leaves unused any excess tokens.

Therefore, in V3, liquidity is not provided directly, but is derived from amount0 / amount1, and different price positions correspond to different asset structures:

| Location | Assets Required |

|---|---|

| The current price is within the range | token0 + token1 |

| Price is below range | Only token0 is needed |

| The price is above the range | Only token1 is needed |

For the specific calculation formula, please refer to section 4, "Calculation of Liquidity ", in "01_Liquidity Mathematical Expressions".

4. Add position: increaseLiquidity

The essence is to add liquidity within the same price range.

- The interval

tickLower / tickUpperremains unchanged - Requires additional investment in tokens

- Mathematically, the new liquidity is still derived based on the current price , the range and the new

amount0 / amount1 - If the price is within the range, you need to consider the constraints on both sides of token0 / token1 at the same time, and finally choose the smaller liquidity that the two can support.

- If the price is outside the range, it will degenerate into a unilateral asset to increase liquidity.

In terms of contract implementation, increaseLiquidity first calls LiquidityAmounts.getLiquidityForAmounts(...) to calculate how much liquidity can be added based on the current price and input amount. Before increasing liquidity, the fees that have accumulated but have not yet been recorded in the current position are settled first, and then liquidity is updated and pool.mint(...) is called to complete the increase. For the calculation formula, see "01_Liquidity Mathematical Expressions" - section 4, "Calculation of Liquidity ".

5. Reduce position: decreaseLiquidity

The opposite of adding a position is removing part of the liquidity from the current position.

liquiditydecreases- The corresponding part of the token is released

- But it will not be automatically transferred to the user's wallet, so a subsequent call to

collectis required.

Mathematically, it's still based on the same set of V3 liquidity formulas, just in the opposite direction:

- Add position:

amount0 / amount1 -> liquidity - Reduce position:

liquidity -> amount0 / amount1

In terms of contract implementation, decreaseLiquidity directly calls burn(...) on the pool, and the core settles the amount0 / amount1 corresponding to the liquidity removed based on the current price position and range. The calculation formula can be found in "01_Liquidity Mathematical Expressions" - section 4.2, "Calculating the Token Amounts from Liquidity".

It should be noted that fees must be calculated once when adding or reducing a position, because V3 fees are not collected automatically in real time. Instead, they are accounted for through the feeGrowthInsideLastX128 + tokensOwed snapshot-and-delayed-settlement method.

Therefore, when increaseLiquidity, decreaseLiquidity, or collect is called, the contract first performs fee settlement. Based on the current feeGrowthInside, it calculates the new fees accumulated since the last snapshot and adds them to tokensOwed. It then updates liquidity or processes withdrawals. Otherwise, fees earned by the old position would be lost, and newly added liquidity would incorrectly share historical fees.

However, these fees are not transferred out automatically; they must be claimed through a later collect operation. So how are these fees calculated and allocated precisely? How does collect transfer these benefits to users? That is the core topic of the next chapter.